Understanding Your Cash Conversion Cycle Without a Finance Degree

Most business owners understand sales, margins, and revenue.

But the metric that often determines whether a company can actually grow without running out of cash?

Your cash conversion cycle (CCC).

And here’s the truth:

You don’t need a finance degree to understand it.

You don’t need complex spreadsheets to track it.

But you do need to understand it if you want to scale confidently in 2026.

This is Real Talk Finance, breaking down financial concepts in plain English so business owners can make smarter decisions.

Let’s start with the basics.

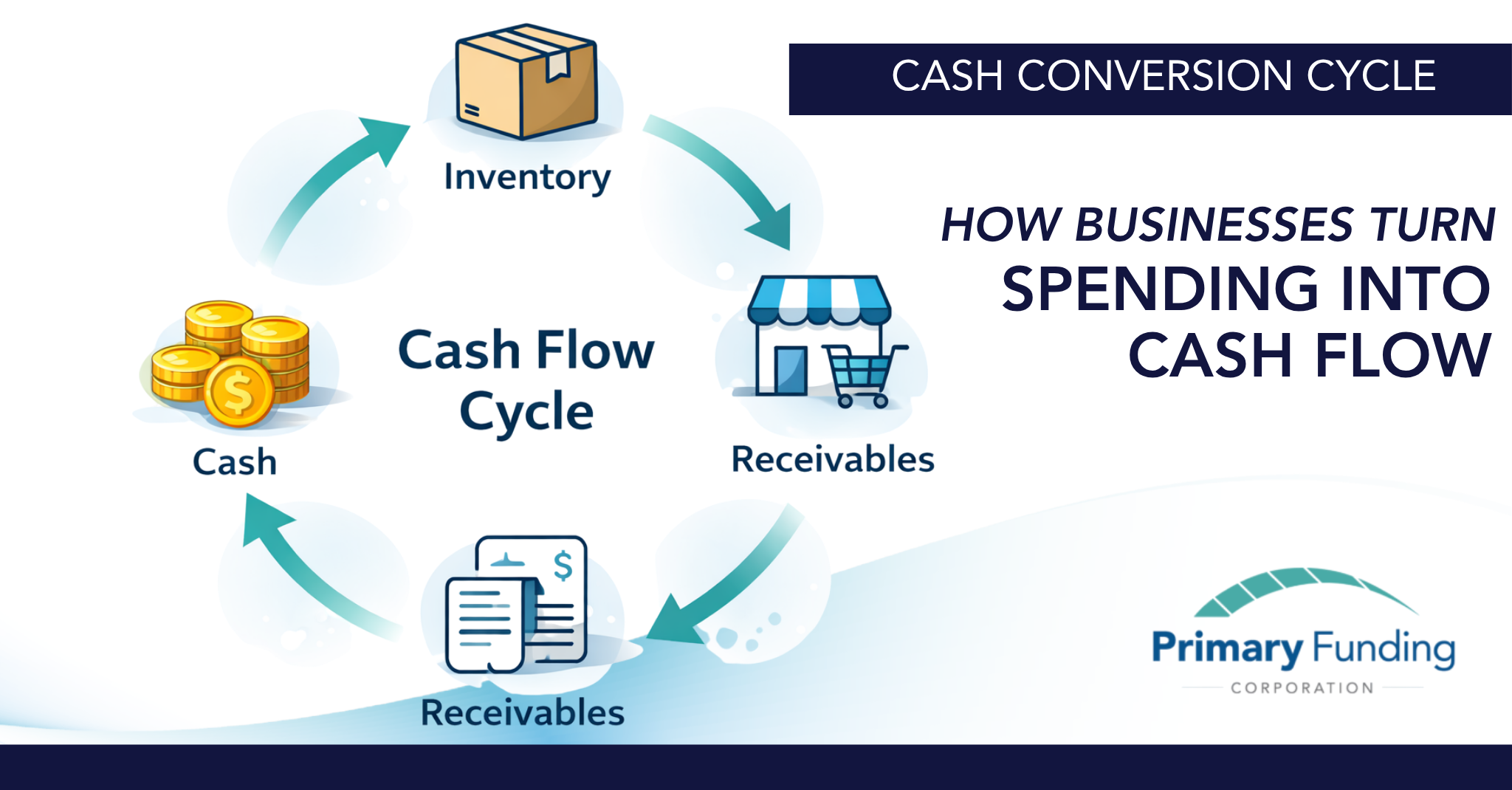

What Is the Cash Conversion Cycle?

The cash conversion cycle measures how long it takes for your business to turn money spent into money received.

In other words:

How long does your cash stay tied up before it comes back to your bank account?

Every business spends money before it gets paid. The cash conversion cycle simply measures how long that process takes.

The cycle includes three main components:

1. Days Inventory Outstanding (DIO)

This measures how long inventory sits before it is sold.

For manufacturers and distributors, inventory may sit in warehouses, production lines, or shipping queues before generating revenue.

The longer the inventory sits, the longer cash remains tied up.

2. Days Sales Outstanding (DSO)

This measures how long it takes customers to pay after you send an invoice.

If your payment terms are net 30, net 60, or even net 90, your business may be waiting months before revenue actually becomes cash.

3. Days Payables Outstanding (DPO)

This measures how long your business takes to pay suppliers.

Longer supplier terms can help balance cash flow by giving you more time before money leaves your business.

The Formula

The formula itself is simple:

Cash Conversion Cycle = DIO + DSO – DPO

But the value of the CCC isn’t the math.

It’s what the number reveals about how your business uses cash.

Why the Cash Conversion Cycle Matters More Than Revenue

Revenue growth alone doesn’t guarantee financial stability.

A business can:

- Land its biggest contract ever

- Increase orders dramatically

- Expand into new markets

…and still struggle with cash flow.

Why?

Because growth often extends the cash conversion cycle.

Here’s what that looks like:

Short CCC:

Cash moves quickly through the business, making growth easier to sustain.

Long CCC:

Cash stays tied up longer, slowing momentum and increasing financial pressure.

In industries like manufacturing, wholesale distribution, and staffing, the cash conversion cycle often increases as the business grows.

Ironically, more success can mean more cash tied up in operations.

Real Examples Business Owners Recognize

Understanding the cash conversion cycle becomes much clearer when you look at real-world scenarios.

Distributors

Distributors often purchase inventory weeks or months before it sells.

Even after products are delivered, customers may take 30–60 days to pay invoices.

The CCC reveals how long the capital is locked in the process.

Manufacturers

Manufacturers purchase raw materials, run production cycles, ship finished goods, and then wait for payment.

The cash conversion cycle shows how much working capital is required to maintain production at scale.

Staffing Companies

Staffing firms often run weekly payroll but may not receive payment from clients for 30–60 days.

This creates a predictable but challenging timing gap between payroll and receivables.

The CCC helps quantify that gap.

How Businesses Can Shorten the Cash Conversion Cycle

Even small improvements in the cash conversion cycle can unlock significant working capital.

Here are three practical ways businesses reduce their CCC.

Improve Receivables Collection (DSO)

Speed up how quickly customers pay.

Practical steps include:

- Sending invoices immediately

- Following up before invoices become overdue

- Offering early payment incentives

- Using receivables financing to convert invoices into same-day cash

Optimize Inventory (DIO)

Inventory management plays a major role in the CCC.

Businesses can improve efficiency by:

- Forecasting demand more accurately

- Reducing slow-moving inventory

- Aligning purchasing with actual order patterns

Work Strategically With Suppliers (DPO)

Strong supplier relationships can help extend payment timelines.

Businesses may benefit from:

- Negotiating longer payment terms

- Aligning purchasing cycles with incoming revenue

- Building long-term supplier partnerships

Where Working Capital Financing Helps

In many industries, the cash conversion cycle will naturally be longer than the cash a business has on hand, especially during growth periods.

That’s where flexible working capital solutions can help.

Receivables-based financing allows businesses to:

- Turn outstanding invoices into immediate cash

- Smooth the timing gap between payables and receivables

- Continue growing without waiting on slow-paying customers

When used strategically, financing can effectively shorten the operational impact of a long cash conversion cycle.

Real Talk: Why Understanding CCC Matters

You don’t need to be a financial expert to understand your cash conversion cycle.

You just need clarity on three things:

- How long does cash stay, tied up

- Where delays happen in the cycle

- Which levers shorten the timeline

For business owners planning growth in 2026, understanding the cash conversion cycle will be a helpful competitive advantage.

Because when you understand how cash actually moves through your business, you can plan growth with far greater confidence.

And in business, clarity creates momentum.